![]()

Don’t fight this bull. It could destroy your future.

Don’t fight this bull. It could destroy your future.

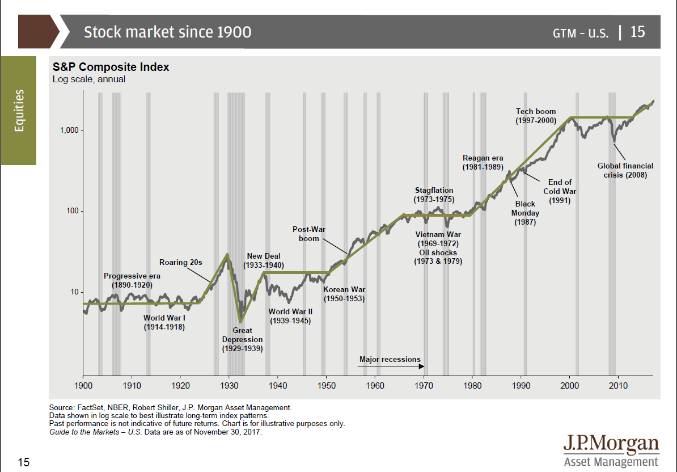

The Dotcom Bubble burst in early 2000, killing the last secular bull market. Since then, we have had two major bear markets, one driven by economics and the other by financial panic. As recently as 2013, the stock marketi was lower than where it opened this century. The S&P Index closed the 20th Century at 1469.25 and last closed below that level about five years ago, on January 9, 2013.

People have long memories of pain, probably outweighing their desires for gain. According to John Piccard of JP Morganii, net cash flows of US equity mutual funds AND ETFs remain negative despite eight years of expansion following the crash. In other words, more money is flowing out of the stock market than into it through these vehicles.

Conversely, the bond market flows are positive. Remember, bonds pay interest but have prices that move the opposite direction of interest rates. Who knows which way interest rates are heading?

Here’s where ignoring the bull could destroy your future.

If you still measure your life expectancy in decades, in other words, you are healthy and in your sixties or younger; you need to be concerned about inflation. Inflation erodes buying power. With just 3% inflation, according to the rule of 72, costs double in 24 years. Put another way; it takes twice as much money in 24 years to maintain today’s standard of living.

Secular bull markets create tremendous wealth as the stock market grows by a magnitude of four or five times like it did during the 1950’s and 1980’s.

Secular bull markets create tremendous wealth as the stock market grows by a magnitude of four or five times like it did during the 1950’s and 1980’s.

The case supporting a secular bull market breakout is fascinating, if not overwhelming. Factors include near record low volatility, earnings-driven global expansion, weening off monetary stimulus, and regulatory relief.

A simple but effective measure of volatility is counting the number of days the market moved by more than one percent. As of this writing, 2017 is on track to be the third least volatile year since 1950. While there is only a slightly inverse correlation between volatility and returns, the two years with lower volatility experienced double-digit gains.

Another measure of volatility is the number of 5% downturns. In a typical year, we expect about three such events. Since February 2016 there has been nothing approaching even this modest level of contraction. In fact, just the opposite occurred. Through November the market broke its all-time high 58 times in 2017.

This expansion started over eight years ago, so many pundits argue it is already past its prime. However, the anemic pace of the recovery (see our June 2016 “Flaccid Recovery” video) logically implies that it should be an exceptionally long recovery. There is a significant stimulus transition in-process. Monetary policy which around the world drove investments for years is giving way to fiscal policy as business-friendly lawmakers reshape tax policies and regulatory procedures.

Companies around the world are making money at record levels, posting a 19% earnings gain over the past 12 months. Virtually all the stock price gains in the Eurozone and Japan are attributed to earnings growth, while 70% of emerging markets gains are attributed to earnings growth.iii

Global growth is good for American companies, too. During the recently ended third quarter, companies with more than half of their revenues from overseas expanded earnings by 13.4% from the previous year while their more domestic counterparts gained only 2.3%.iv

The case against a secular bull market is lame. High trailing P/E’s are typical of the current interest rate and inflation environments. Corporate earnings overcame a highly touted “earnings recession” and US tax reform is likely to convert headwinds to tailwinds.

While we often measure economic cycles in quarters, secular markets transcend these periods often including significant downturns. There were at least two significant recessions during both the previous secular bulls, not to mention multiple geopolitical events.

Likewise, volatility is a regular part of markets. Only periods of extremely high volatility show a significant correlation to market performance. More importantly, correlation is not the same as causation, and I believe that fear and panic are as much a cause of volatility as a result of it.

According to Piccard, trailing Price to Earnings (P/E) ratios typically run high during periods of low inflation and low interest rates. There are few good alternatives to stocks when bonds pay so little. Moreover, while the P/E ratios are on the high side of average, the increased earnings expected in the future, enhanced by the tax law changes, are nowhere near bubble status.

There are always risks when investing, many are seen only in hindsight. However, for long-run investors now is the time to overweight equity exposure as the near term appears to favor stocks over fixed income investments. Contact us to review your portfolio for specific recommendations that should align with your long-run goals and investment objectives.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

Investing involves risk including loss of principal. No strategy assures success or protects against loss.

i Unless otherwise noted, references to the stock market valuation is as measured by the S&P 500 Index, an unmanaged index into which individuals cannot invest directly.

iiJP Morgan Asset Management Equity Strategist John Piccard visited our offices on January 7 and discussed his research and strategies.

iiihttps://www.wsj.com/articles/global-earnings-record-offers-hope-that-rally-will-continue-1512455401

ivhttps://www.wsj.com/articles/economy-has-room-to-grow-heres-why-1512309600

TRACKING # 1-677183