![]()

What do the Watts Riots, Beatlemania, Kennedy’s Assassination, ZIP Codes, the Vietnam War, Cassius Clay’s first World Heavyweight Championship, South African Apartheid and Nelson Mandela’s lifetime prison sentence, Buffalo Wings, Martin Luther King’s “dream” speech and march from Selma to Montgomery, the Ford Mustang, a power blackout stretching from New Jersey into Canada, and creation of the word “hypertext” have in common?

What do the Watts Riots, Beatlemania, Kennedy’s Assassination, ZIP Codes, the Vietnam War, Cassius Clay’s first World Heavyweight Championship, South African Apartheid and Nelson Mandela’s lifetime prison sentence, Buffalo Wings, Martin Luther King’s “dream” speech and march from Selma to Montgomery, the Ford Mustang, a power blackout stretching from New Jersey into Canada, and creation of the word “hypertext” have in common?

They all appeared during the three least volatile years of the stock market, as measured by the number of 1% daily moves in either direction of the S&P 500 Index.1

However, the period also produced Bob Dylan’s “The Times They Are a-Changin,” and indeed they were. There wasn’t another year with similar low volatility until 2017, which now stands as the second most stable year in the history of the S&P 500 Index.

However, the low volatility ended abruptly in February 2018 as the market careened into correction territory taking just nine trading days to fall more than 10% from an all-time high of 2873 on January 26 to close on February 8 at 2581.

What caused the carnage?

In my opinion, this correction was caused by the same kind of behavior that triggered the last one following the collapse of oil prices, bottoming-out February 11, 2016. But the energy sector is not to blame, in either of these episodes. Computers, speculation, and leverage are the culprit.

Here is what happened both times. Prices developed a steady and consistent trend. Speculators, recognizing that “the trend is your friend” saw an opportunity two years ago to bet against oil prices falling and more recently against a spike in volatility. In both cases, it did not take much for the speculators to fear a change against their highly-leveraged positions and once that happened, the computers kicked into selling mode driving down the markets.

Ironically, it was good news that triggered this correction. The economy is at nearly full employment and wages are beginning to rise. Corporate profits are healthy, and the recent tax bill improves them going forward. With all these good things happening, inflation is most likely to increase.

Typically, the FED raises the Federal Funds rate to fight inflation and the markets expected a moderate rate of these increases. However, the improved economic data implied those increases might come faster than the markets expected, and the selloff began.

Going forward, I predict that market volatility will return to its long-run averages. Using the same measure of movement more than 1% either way in each day, over the history of the S&P 500 index, that happens on average about once per week. Of course, it will come in spurts, with periods of calm interspersed with periods of storms.

Don’t think that increased volatility is dangerous for investors. Short-term unpredictability gives the traders opportunities to earn and lose lots of money, quickly. It also gets people out of the markets who have no business trading, unfortunately for some, by wiping out their capital. However, long-run investors must embrace these same risks if they hope to accumulate and maintain real wealth and buying power.

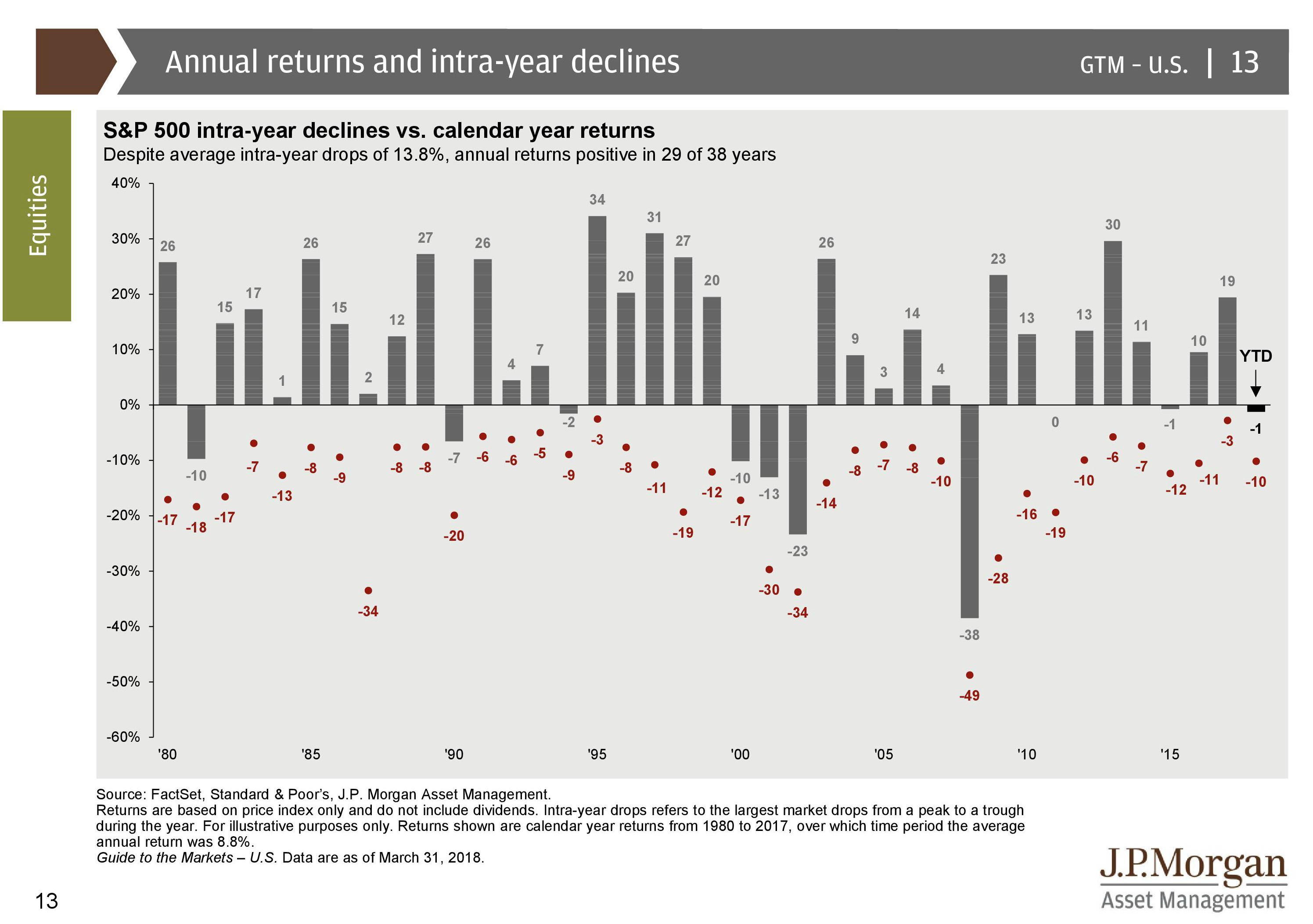

When the volatility returned in February, it erased the market’s 5.62% January gain. Rarely does a year that begins with a positive return for the month of January end the year losing ground. In fact, in the history of the S&P 500, it has never been negative in a calendar year that did 3.5% or better in January. However, in all those years there was a significant intra-year sell-off.

Nine times since 1980 the market gained between 3.5% and 7.5% in January, with an average 5.4% gain.2 The average intra-year drawdown, according to the following chart from JP Morgan is 9.8%, making the 5.6% January 2018 gain and the 10.2% February 2018 drawdown just about average for this data set.

You should now be wondering how well the market performed during this select group of years. The price performance of the S&P 500 index in the ten years with January returns between 3.5% and 7.5% is a very respectable 22.9% with a low of 12.4% in 1988 and a high of 31.0% in 1997.

Past performance is no guarantee of future returns, and you cannot invest directly into an index, but is it reassuring to know that history is on the side of success.

There are challenges, of course. The economy is in the latter stages of a historically long but anemic expansion, which led to the massive political and regulatory changes seen recently in the USA. It is impossible to predict what is likely to come out of Washington confidently, and there are always unpredictable events which can destabilize the world.

However, it is also reasonable to assume that businesses will adapt to changes in the economic climate to the benefit of their shareholders. Therefore, we continue to encourage investing in balanced portfolios tailored to individual goals and risk tolerances. Call us to learn how we can help you pursue your financial objectives.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

1There were 19 trading days with moves over 1%, spread over 756 trading days during the years 1963-65.

21987 appears as an anomaly as January gained 13.2%, almost double the next highest return, and contained Black Monday, the stock market crash leading to the creation of “market curbs” or circuit breakers. Program trading likely played a role in the crash, but none-the-less the market returned to positive territory by year end, eking out a 2% price gain.

TRACKING #1-706841