By: Ralph Bender, MBA, CFP®

By: Ralph Bender, MBA, CFP®

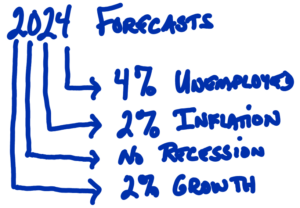

Dr. David Kelly of JP Morgan shared this acronym describing the economy in the new year during the first advisors-only conference call of 2024. In short, he’s optimistic about the coming year. He is known for basing his opinions on consistently sourced quantifiable data. Of course, unexpected events cannot be reliably predicted and could dramatically change the economic landscape.

So, plan for the unexpected.

Here’s how:

Maintain emergency reserves. Somewhere between three and six months of your known expenses should be immediately accessible, probably in an insured bank account.

Eliminate bad debt balances. Bad debt is a rolling credit card balance or a Home Equity Loan that didn’t increase the value of your property but rather expanded your lifestyle spending.

Rebalance your portfolio. Take profits from overpriced asset classes. In the recent past, the valuations of the equity market leaders became “rich” compared to historical averages. Use the profits to add to their underpriced counterparts. Bond assets and most publicly traded companies reverted to valuations closer to historical norms.

Rebalancing a portfolio of stocks and bonds following a year like 2023 is a prudent way to adjust the risk/reward profile, and it is a service we provide for our advisory clients.

Dr. Kelly’s forecast implies a normal economy moving into this new year. All four of the components’ forecasts appear both achievable and sustainable.

Growth. Gross Domestic Product (GDP) measures economic growth. Labor is a prime component, and labor force participation rates among traditional working-age Americans are at a 14-year high. These workers and their employers use technology to increase efficiency and effectiveness, thereby increasing productivity.

Recession. Talk of recession flipped from the majority to minority opinion late last year, reinforced by the FED’s move from hawkish to dovish on future interest rate hikes. We’ve maintained that recession fears didn’t align with reality for most of the past two years. I’m still optimistic.

Inflation. Published readings of the nations’ inflation, especially the Consumer Price Index (CPI) factor in housing costs. Owning a home, even with a fixed-rate mortgage, locks in the housing expense and is an example of good debt. For people who aren’t moving, aren’t renting, and aren’t using adjustable-rate mortgages, this inflation component should be removed to get a relevant number. Currently, it’s the main culprit slowing the inflation rate decline. Dr. Kelly believes that as the housing costs normalize, we’ll likely see even the CPI hit the FED’s targeted 2% rate, soon.

The rest of the core inflation components achieved normal rates as the supply chains normalized. Food and energy costs don’t get included in core inflation, as they both have relatively fixed demand, so any change in supply can whipsaw prices.

Unemployment. The labor market remains strong, yet not so strong that companies push up wages dramatically. Like the other factors, 4% of workers seeking work is typical of a normal economy.

And while it is an election year, that’s rarely stopped businesses from generating profits. And we invest in businesses, not politicians.

As always, we welcome your questions, and of course, we covet your referrals.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Rebalancing a portfolio may cause investors to incur tax liabilities and/or transaction costs and does not assure a profit or protect against a loss.

Stock investing includes risks, including fluctuating prices and loss of principal.

Bonds are subject to credit, market, and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

Tracking #523893-1