“What’s happening to my portfolio? Should we move into more conservative investments?”

That’s a common refrain since the beginning of the year, and it’s something we didn’t hear at all since the early days of Covid stimulus packages. That’s because following the steepest downturn in recent stock market history, the market rebounded and simply kept climbing. People lost perspective on what to expect from the markets.

So, let’s set the record straight.

Over long periods, measured in decades, not days, weeks, or years, the stock market returns about 10% annually (as measured by the S&P 500 Index – excessive disclosures and disclaimers in the footnotes)[ The S&P 500 is an unmanaged index which cannot be invested into directly. Past performance is no guarantee of future results. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.]. In exchange for that very nice return, investors are expected to endure pullbacks of 5% or more three times every year, and at least one 10% correction every year.

But what happened in 2021?

There are 252 trading days in a calendar year. Those are days the stock market is open for business. In 2021, on 70 of those days, more than once per week, the market closed at an all-time high. It never had a drop much bigger than 3%, because it was so busy climbing about 28% for the whole year.

Guess when it had its last all-time high.

January 3, the first trading day of 2022. And since then, it’s been mostly in retreat. It dropped to minus 13% in mid-March, then rebounded to about minus 3%, before heading back down into “correction” territory, minus 10% or more.

So, the behavior of the stock market is pretty normal.

What makes this situation a bit more difficult to swallow is what’s happening in the bond markets[ Government bonds and Treasury Bills are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.]. Bonds are usually considered the safer side of a portfolio. But now they’re probably causing most of the discomfort.

We’ve seen and heard that interest rates are headed up. What we don’t know is how high they’re going.

Brief note on bond prices: when interest rates rise, bond prices fall. It’s mathematical, so no need to wax eloquent about it.

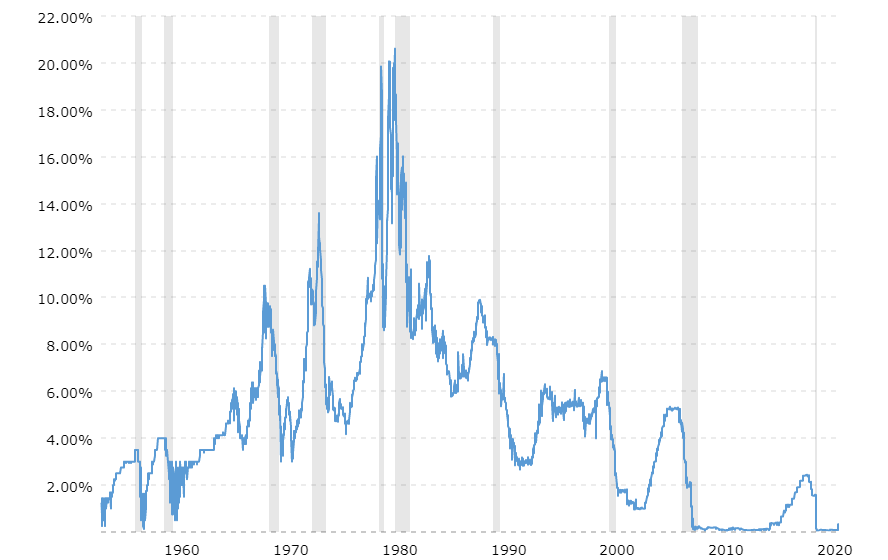

Bond prices are falling because investors are anticipating, according to my Goldman Sachs rep, eleven future FED rate hikes. At 25 basis points, 11 rate hikes put the FED Funds rate at 3%. As you can see in the chart, we haven’t seen it that high since 2008[ For an interactive version of the FED Funds Rate Chart displayed, go to: www.macrotrends.net/2015/fed-funds-rate-historical-chart’]. But for most of the five previous decades it rarely dipped below 3%.

So, both bonds and stocks headed down. At the same time. And that’s not what’s expected, but it’s not unprecedented. But in bonds, in my humble opinion, the market is pricing for the worst case, which isn’t likely to occur.

As always, contact us with any questions or concerns about your portfolio’s ability to help you confidently discover and pursue your dreams.

TRACKING #35360-1