A client recently asked a question I hear regularly. The names have been changed, but the situation is common enough that the answer is worth sharing publicly.

A client recently asked a question I hear regularly. The names have been changed, but the situation is common enough that the answer is worth sharing publicly.

Q: My wife Frances just turned 63. Some of her colleagues are encouraging her to claim her Social Security benefit now and then switch to a survivor benefit on my record when I pass. She plans to keep working part-time. What should we consider?

A: This is a genuinely complex question, Thomas — and Frances’s colleagues aren’t entirely wrong. But there’s quite a bit more to untangle before deciding.

The three benefits Frances could receive

Frances has access to three distinct Social Security benefits, and they interact in ways that aren’t always obvious.

Her own benefit is based on her personal earnings record. A spousal benefit — available once you file — would top up her benefit to 50% of your age 67 (aka Full Retirement Age (FRA)) benefit, minus her own age 67 benefit. And the survivor benefit is the one her colleagues mentioned: if you predecease her, she receives the greater of her benefit or yours, not both.

For the spousal and survivor benefits, your benefit amount matters enormously. In your case, Thomas, you’ve been at or near the Social Security taxable wage base for most of your career. That shapes your benefit significantly — and makes the math worth running carefully.

What claiming at 63 actually costs

Claiming four years before age 67 reduces Frances’s own benefit by approximately 25% and her spousal top-up by approximately 30%. These aren’t temporary reductions. They’re permanent, and every future cost-of-living adjustment (COLA) compounds them.

Here’s an illustrative example. Say your age 67 benefit is $4,000 monthly and Frances’s is $1,000. Her spousal top-up at age 67 would be $1,000 (half of your $4,000 = $2,000, minus her own $1,000 benefit). Claiming at 63 reduces her own benefit to about $750 and the spousal top-up to about $700 — a total of $1,450 monthly instead of $2,000.

Here’s an illustrative example. Say your age 67 benefit is $4,000 monthly and Frances’s is $1,000. Her spousal top-up at age 67 would be $1,000 (half of your $4,000 = $2,000, minus her own $1,000 benefit). Claiming at 63 reduces her own benefit to about $750 and the spousal top-up to about $700 — a total of $1,450 monthly instead of $2,000.

By the time Frances reaches her mid-70s, the larger monthly benefits from delaying have overtaken the balances

received by claiming early. By her mid-80s, she’s about $65,000 ahead by delaying, and that grows to about $140,000 if you both live to your mid-90s.

These numbers use the illustrative benefit amounts above. The only way to know the real numbers is to have your actual Social Security Statements in hand.

The earnings test: why working changes the math

Frances still plans to work, and that matters. In 2026, the Annual Earnings Test (AET) exemption is $24,480. If she earns more than that before reaching age 67, Social Security withholds $1 in benefits for every $2 of excess earnings. Withheld benefits aren’t lost forever — they get credited back as a slightly higher benefit at age 67 — but it complicates cash flow planning and reduces the near-term value of claiming early.

If Frances’s income stays around $24,000–$25,000 annually, she likely stays within the exempt amount, and the earnings test isn’t a significant concern.

The case for claiming early

There is one. If she claims now and stays below the AET limit, she’d collect roughly $750 monthly for four years — approximately $36,000 in cumulative benefits before any COLA adjustments. If she can invest those proceeds — particularly in a Roth IRA, since she has earned income — the case becomes stronger, as tax-free compounding adds real value to the early-claiming strategy.

The case for waiting

Our general planning philosophy treats delayed Social Security claiming as longevity insurance. It’s a government-guaranteed benefit, indexed to inflation, that neither of you can outlive. The survivor receives the full amount — which is especially meaningful for a surviving spouse facing potentially 25 to 30 years on a single income.

Because you’re the higher earner, Thomas, the most important long-term move is for you to delay to 70. That maximizes the benefit Frances would receive as your survivor for potentially decades. Staying active and healthy — as we discussed in Stay in Your Prime Longer: Why Active Retirees Enjoy 15 More Years of Independence — directly affects how long that survivor benefit matters, which is why the two decisions are connected.

For Frances specifically, whether delaying her own benefit is worth it depends on how large that benefit actually is, how it interacts with the spousal top-up, and what bridge income you’d use in the meantime. Which brings us back to the Statements.

A security note worth acting on today

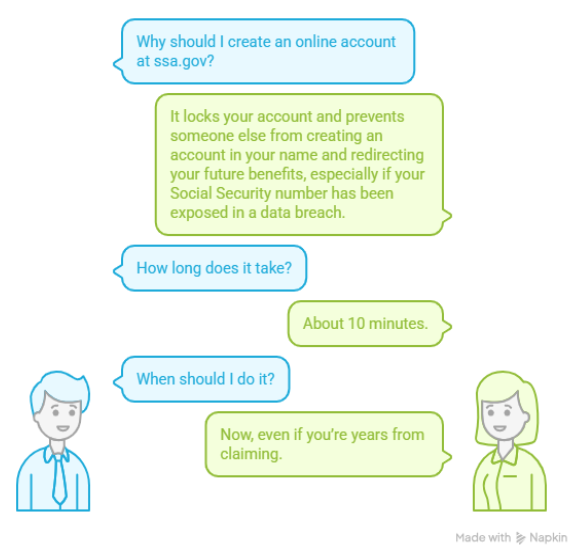

If either of you has never created an online account at ssa.gov, do it now — even if you’re years from claiming. Once your Social Security number has been exposed in a data breach (and statistically, it probably has been), someone else could create an account in your name and redirect your future benefits. Creating your account first locks it. It takes about 10 minutes and is one of the simplest protective steps you can take.

What we’d want to know before finalizing anything

Leading academic research — and the Social Security Administration itself — has found that for people with normal life expectancies, the lifetime value of benefits is roughly similar across claiming ages. The difference comes down to longevity assumptions, investment returns, and how the survivor benefit interacts with each strategy. Since both of you expect long lives, delayed claiming tends to come out ahead once survivor protection is factored in.

But we can’t actually know which strategy works better for your household without Frances’s projected benefit, your projected benefit, and the numbers from your Social Security Statements. If you don’t have them handy, we can access them together. That 20-minute conversation could be worth six figures over a lifetime.

Research and development of this article involved AI tools; graphics were AI-generated.