Sam Darnold, like each of his Seahawk teammates, earned $178,000 by winning Super Bowl LX in Santa Clara, California, following the 2025 NFL season. The eight days he worked in California will cost him about $249,000 in California Income Tax.

Sam Darnold, like each of his Seahawk teammates, earned $178,000 by winning Super Bowl LX in Santa Clara, California, following the 2025 NFL season. The eight days he worked in California will cost him about $249,000 in California Income Tax.

Ouch!

You’re probably not earning Sam Darnold’s salary. But if you’re a high-earning professional who travels to conferences, client meetings, or training events — especially in California or New York — the same legal mechanism that produced his tax bill may apply to you.

Say what?

It’s Not Just Athletes

California and most other states tax income earned within their borders by anyone — resident or not. For athletes, this is called the “Jock Tax,” and it’s calculated using a duty-day formula: the number of days you perform work-related activities in the state, divided by your total working days for the year, multiplied by your total compensation.

The same sourcing rules apply to corporate employees, consultants, sales executives, engineers, and anyone else whose employer sends them to California for work — including conferences.

California Hosts the World’s Biggest Professional Conferences

Consider what’s held in California every year: Salesforce Dreamforce draws tens of thousands of technology professionals to San Francisco. Adobe MAX fills Los Angeles. BIO International Conference brings life sciences executives to San Diego. The Milken Institute Global Conference hosts financial and business leaders in Beverly Hills. Future Proof — one of the largest financial advisor conferences in the country — runs annually in Huntington Beach.

Tens of thousands of out-of-state professionals attend these events each year. Most of them have no idea they may be creating a California tax filing obligation by doing so.

The Rate That Surprises People

Here’s the part that isn’t intuitive. California doesn’t tax your conference days at the rate you’d pay if $15,000 or $20,000 were your only income. It calculates the effective tax rate based on your total worldwide income, then applies that rate to your California-source income.

The legal rationale, upheld by California courts, is that taxpayers with equal total incomes should be taxed at equal rates, regardless of how much of that income was earned in-state. A nonresident earning $20,000 in California and $380,000 elsewhere is taxed at the same effective rate as a California resident earning $400,000.

In practice, for a high earner, that means California conference days are taxed at something close to California’s top rate — not the lower rate that would apply if the California income were viewed in isolation.

Example: The Conference Attendee

Marcus is a 42-year-old senior sales engineer at a Texas-based technology company earning $230,000. His wife teaches at a private school in Texas, earning $55,000. They file jointly. His company sends him to a four-day industry conference in San Francisco each spring and a two-day product summit in Los Angeles each fall — six California duty days, plus two travel days, for a California footprint of roughly eight days out of approximately 220 working days for the year.

California duty days / Total working days = 8 / 220 = 3.6%

3.6% × $230,000 = approximately $8,300 in California-source income

California sets the effective tax rate based on the full household income: $285,000 MFJ

Effective California rate on $285,000 MFJ: approximately 10.5%

Estimated California tax: $8,300 × 10.5% = approximately $870

Marcus and his wife live in Texas — no state income tax, no offsetting credit. They owe California $870, have likely never filed a California return, and almost certainly don’t know it.

Where You Travel Matters

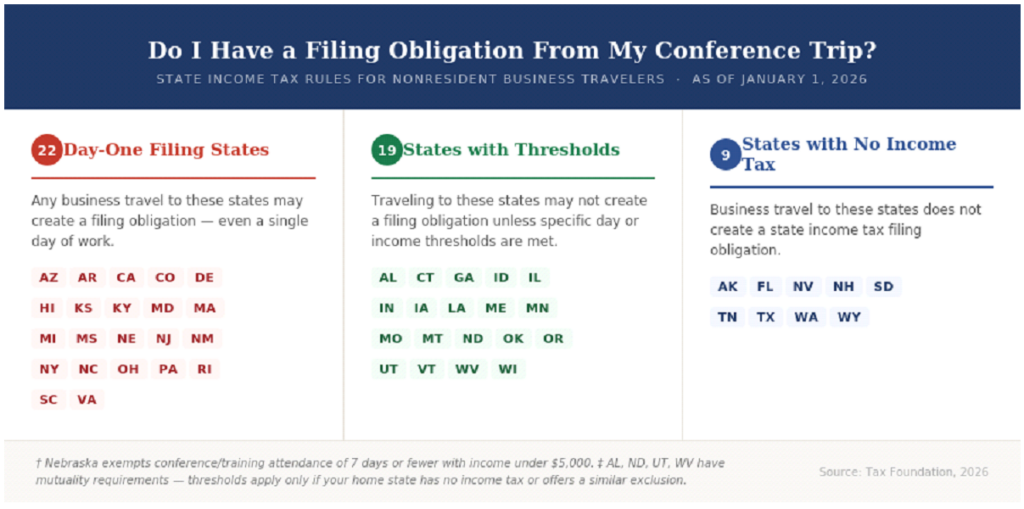

California and New York are the highest-stakes destinations for out-of-state professionals — top tax rates, aggressive enforcement, and no day-one grace period.

But they’re not alone. As of 2026, 22 states technically require a non-resident to file after a single day of work in the state. Most states will offset any tax paid to another state, avoiding double taxation.

Where Equity Compensation Makes It Much Bigger

For most conference attendees, the California tax exposure is a footnote, but for executives with equity compensation, it can become a headline.

California taxes RSUs based on how many of your workdays during the grant-to-vest period were in California. When the shares vest, that ratio is applied to the ordinary income recognized — even if you’ve long since moved away.

Non-Qualified Stock Options (NSO) work the same, but the dates run from grant to exercise. In many cases, the vesting might be four years with the option to exercise up to six more years. The State of California can use all your workdays in California during those 10 years to calculate your tax liability.

Incentive Stock Options (ISOs) are even more complex and beyond the scope of this article, but California expects their share based on your workdays.

What to Do About It

The professional value of attending industry conferences typically far outweighs the tax exposure. A few straightforward habits can keep you informed and prepared.

- Archive your business travel calendar with your tax returns every year. Online calendars often roll off prior-year data. Before that happens, export or screenshot your calendar and save it alongside your tax records. Dates, cities, and meeting purpose are your documentation if a state ever questions your day allocation. Tell your preparer where you traveled and for how long; don’t wait to be asked.

- If you have equity compensation and have worked in California during a vesting period, get a specialist review. Liability can be substantial and doesn’t announce itself.

A note on practical reality: California’s Franchise Tax Board is not likely to pursue an $870 liability from a single conference. But the FTB is formidable when it does act — it receives IRS data feeds, runs automated bank-matching programs, and has 20 years to collect once a liability is assessed. For non-filers, there is no statute of limitations. The exposure that warrants real attention is equity compensation, frequent multi-state travel, or California income above a few thousand dollars annually. Below that, awareness is reasonable; losing sleep is not.

The Broader Point

Sam Darnold’s Super Bowl tax bill is extreme because his salary is extreme. But the underlying mechanics — duty-day sourcing, worldwide income rate-setting, no offset for no-income-tax state residents — operate at every income level where cross-state work is involved. The U.S. has no uniform standard. Twenty-two states can claim your income from day one. The rules are dense, and most busy professionals have no idea where they stand.

Tax season is a good time to find out.

Important Disclosures

This content is for educational and informational purposes only and is not intended as tax, legal, or investment advice. Tax laws are complex, change frequently, and vary by individual circumstance. The examples and calculations presented are illustrative only and should not be relied upon for tax filing purposes. Consult a qualified tax professional regarding your specific situation.

Research and development of this article involved AI tools; graphics were AI-generated.