fi·du·ci·ar·y (noun): A person who occupies a position of such power and confidence with regard to the property of another that the law requires them to act solely in the interest of the person whom they represent. — Britannica

Fiduciary has become the current buzzword for doing the right thing in financial services. The idea is sound — you want someone legally required to act in your interest. But a buzzword sets a floor, not a ceiling. Trust is built over time, through the relationship, not the fee structure.

Who Qualifies as a Fiduciary?

Notice that the dictionary definition doesn’t say “financial advisor.” A fiduciary is anyone who holds a position of trust and is legally obligated to act in your interest rather than their own. Attorneys are fiduciaries to their clients. Trustees are fiduciaries to beneficiaries. Corporate board members are fiduciaries to shareholders.

In financial services, the fiduciary obligation applies specifically to advisors continually managing your investments and keeping you informed of the adjustments they make on your behalf — not to everyone who might sell you a financial product.

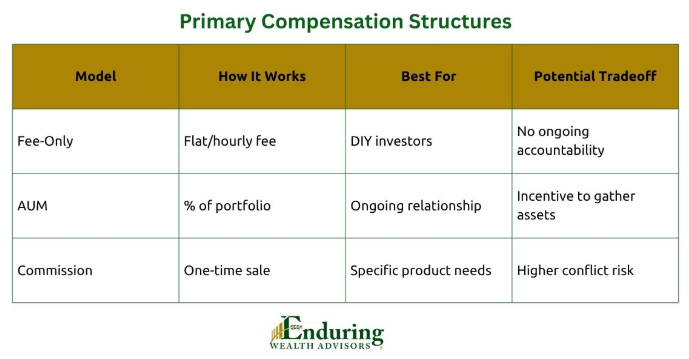

Providing financial advice is a business, and except for start-ups or during occasional downturns, their firm’s revenues must exceed its expenses to remain viable. There are three primary compensation structures in the business: Fee Only, AUM-based Fees, and Sales Commissions.

Each of them can operate within a fiduciary obligation.

Fee-only advisors collect a check from you for their services. You pay them a flat fee or an hourly rate for advice on your issues at that time. It could be to create a financial plan, or maybe something less comprehensive, like evaluating your 401(k) investment

choices. Some charge a retainer under which they can also manage your investment portfolio on an ongoing basis.

The AUM-based fee structure is all about managing the portfolio for the long-run. AUM means “Assets Under Management” and the fee is calculated as a percentage of your portfolio’s value. More money in your account means a bigger fee, while a smaller portfolio pays a smaller fee. Theoretically, this aligns the advisor’s compensation to your experience.

Financial transactions involving illiquid long-term investments like real estate and insurance are prime examples wherein sales charge and commission make the most sense.

Which Advisor Compensation Model is Right for You?

It depends on what you want from the relationship.

If you intend to manage your investments yourself, then perhaps lean into the fee-only design. Write an annual check to an advisor for an annual review, much like many people do with their medical care. If something develops that requires additional expertise, schedule an extra appointment to review the situation. You’re in charge.

While some believe fee-only is the fiduciary gold standard, they are still working for a living, which is done through billable hours. Their conflicts differ from the other models, but so does their accountability – they have no ties to your outcomes.

When – not if – your situation changes, prepare to write another check for their advice.

If you want a more robust relationship, where you have someone working for you, handling the day-to-day details, allowing you to focus on your life goals, the AUM model might work for you.

There are three reasons to consider it. First, the compensation moves with the value of your portfolio. It’s the only model that aligns with your economic outcomes. Second, the relationship is ongoing – guiding you through all sorts of life events. Finally, most AUM models handle the billing directly from the account; you don’t need to write the check.

The risk in this model is the advisor’s drive to become an “asset gatherer” rather than your financial advisor. These advisors farm out all the investment management to TAMPs – Turnkey Asset Management Programs – while they focus on meeting new prospects. That can work, but you should be aware of the advisor’s priorities.

Commission-only salespeople are typically licensed only for the products they intend to sell. Their employers, usually insurance companies, have developed polished presentations featuring the highlights of their products. The required disclosure documents are lengthy, dense, and rarely read – even by the people selling them.

But maybe you just want to get some life insurance to protect your family, or you really want to buy a lifetime income stream through an annuity-based product. Caveat emptor (let the buyer beware) rules in these channels.

What Certification Demands a Fiduciary Obligation?

Besides the licensing, an advisor’s credentials might contain a fiduciary obligation. The industry standard certification for working with the public is the Certified Financial Planner® or CFP®. A CFP® professional – verified through the CFP Board – is trained and tested on most of the categories of life’s financial issues, and unlike most designations you’ll encounter, has a fiduciary obligation over your entire client relationship. When a commission-based product genuinely serves a client’s needs, a CFP® practitioner can recommend and implement it — held to the same fiduciary standard of care that governs every other aspect of the relationship.

Here’s the uncomfortable truth: bad actors use any tool available to deceive you into believing they are acting in your best interest. A legal obligation or an ethics certification doesn’t prevent misconduct — it just defines the standard against which misconduct is measured.

The answer isn’t the licensing or the label, but a structure that keeps an advisor accountable to your relationship.

We Are a Fiduciary Advisory Firm

Our primary compensation is AUM-based fees, which align our financial interests directly with our clients’ long-term outcomes. We also handle short-term engagements on a fee-only basis if that’s what you need. Finally, we maintain the licenses and regulatory oversight needed to work with products that fall outside the advisory world. No matter how you choose to engage with us, the same fiduciary obligation applies.

Our lead advisors hold the Certified Financial Planner® certification, which carries an independent fiduciary obligation covering every aspect of the client relationship – financial planning, tax strategy, insurance, estate planning and retirement income – not just the investment management piece.

We believe the best advisor-client relationships are enduring ones. That belief shapes everything about how we work, how we’re credentialed, and how we’re paid.

If you’re evaluating advisors and want to talk through what our structure would mean for your specific situation, we’d welcome that conversation.

Research and development of this article involved AI tools; graphics were AI-generated.CFP Board owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®, and CFP® (with plaque design) in the U.S.

Tracking# 1121045

Research and development of this article involved AI tools; graphics were AI-generated.

CFP Board owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®, and CFP® (with plaque design) in the U.S.