Why working families need life insurance coverage — now!

Why working families need life insurance coverage — now!

What a new heart attack study means for anyone whose family depends on their income.

A 2025 study published in the Journal of the American Heart Association — and covered by the Wall Street Journal — should get your attention. Adults from 18 to 54 are dying from severe first heart attacks at an increasing rate. And the death toll in this age group from all causes is climbing, too.

While you process what it could mean to your family if they lost you – and your income – please know there’s something potentially worse: surviving, but disabled.

Cardiac disease is the leading killer of Americans. That hasn’t changed in decades, but what has changed is the rates of death. During the decades prior to 2010, according to the National Academies of Sciences, death from all causes among working-age Americans steadily declined (improved). They watch all the causes, including heart disease, drug overdose, alcohol-related illness, suicide, and cancer, and in all cases the trends were the same.

Then came the twenty-tens.

And in America, for the first time in two generations, workers began dying at a faster clip than their predecessors.

Only in America. It’s not happening in any other major developed country.

One data point makes this especially stark: in a 2024 Oxford-Princeton study comparing 25 countries, younger American women ages 25 to 44 were the only group — across all countries studied — whose mortality rate in 2019 was higher than in 1990. In a generation of global health gains, that is a singular and alarming exception.

Death and disability are largely unpredictable. Sure, we make choices that increase or decrease our individual probability of early mortality, but, well, if you’ve known me for a while you know I’ve often said that despite running tens of thousands of miles I could get hit by a truck.

The hard truth is that no one knows the number of their days. And that is financially important, especially when others are dependent on your income. The risk of the loss of your income due to death or disability is the reason for insurance.

The purpose of all forms of insurance is to transfer the risk of the insured “hazard” as the industry calls it, in this case your death or disability, to the insurer. They operate under the law of large numbers, which says that for an individual, there is no known expiration date, but when you work with thousands, or millions, it becomes quite apparent how many deaths will occur in each demographic segment.

Which is what the Wall Street Journal article highlighted. Young working people are dying at an increasing rate.

Grief is difficult. Don’t make it worse by ignoring one of life’s universal truths: memento mori –

you will die. Your income is worth protecting, and it doesn’t matter how much it is if others depend on it.

But here is the good news: if you’re healthy today, protecting that income is surprisingly affordable. Today, a healthy 40-year-old non-smoker can get $1 million in 20-year term life insurance for about $65 a month. Your health and age are primary factors determining the cost, and waiting only gets you closer to your expiration date, so get the insurance in place now.

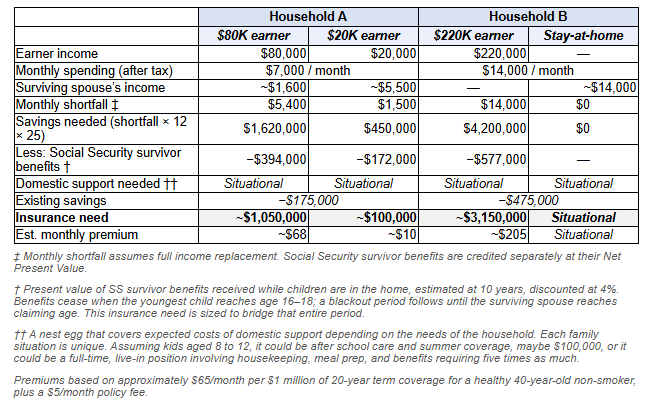

How Much Coverage Do You Actually Need?

The right death benefit isn’t a round number someone picked — it should be calculated. Start with what your family needs monthly to maintain their lifestyle, subtract other income which remains, and that’s the monthly shortfall amount. Multiply a year’s worth by 25 to determine the amount of assets needed. Subtract the value of any Social Security survivor benefits. Adjust for additional needs and existing savings and the result is how much insurance you should buy.

Two hypothetical households illustrate how differently the math works:

When I started financial planning late in the twentieth century, insurance salesmen used a simpler calculation: eight times your earnings. Then I heard that the way to increase sales was to use ten times the earnings. Insurance salespeople are not financial planners; in none of these hypothetical but very realistic examples, does a simple formula like that work, and in fact, it seriously undercuts the recommended death benefits for the primary wage earners.

Another saying from my early years, however, remains true: no beneficiary ever complained

about getting too much life insurance. Simply put, if you insure early and while healthy, rounding up is inexpensive. And it’s a good idea as your next twenty years might be the best earning years of your life.

Or not.

33-year-old David Jeffers dove through an ocean wave, like he’d done hundreds of times before. This time was different. He didn’t see the sand bar but felt it as the force of his dive broke his neck, leaving him a C5/C6 quadriplegic with a young family.

What happened next — medically and professionally — is a story David has told publicly and generously. The financial chapter, we hope to explore with him directly in a future post focused on disability-related planning.

Back to life insurance.

So far, we’ve demonstrated how to determine the death-benefit (amount of insurance) you should consider, and why. And we’ve focused on low-cost term insurance as a satisfactory solution for most working people early in their careers. But there is another broad category of life insurance known by many names. What sets it apart from term, is that it can be permanent, meaning it can be in place for the rest of your life, no matter how long you live.

Here is a basic truth about all life insurance: your risk of dying increases every day you are alive. As Pink Floyd lamented in the song “Time” – every day lived is a day closer to your end. And while something like David’s disability creates a new lifestyle paradigm, any major injury or illness tends to accelerate your mortality, at least in the eyes of insurance company underwriters.

That’s why “whole life” was created (before the US Civil War) to provide a death benefit for when a person dies as opposed to if they die within a specified time period. The key difference is that a savings or investment bucket is added to the policy structure, and it is designed to help pay the ongoing insurance expenses as time marches forward. Early premium rates are very high compared to their term alternatives and the difference between them is used to build the investment bucket (called cash value).

Permanent life policies have some incredible tax advantages, and lots of very sophisticated financial planning strategies can be built around them. But in my experience, for most people and for the most common planning objective, there are other more efficient approaches to reaching financial goals. In short, if you’re still working for a living and others are dependent on your income, insure your life for the length of time you expect to continue earning your living.

And if you’re fortunate enough to create estate planning problems due to your overwhelming financial success, we can talk about some of those sophisticated planning strategies for which permanent life might be considered.

The cardiac data should prompt you to ask yourself, what if something catastrophic happens to my family? Your income might be your only financial asset today. The tool for removing the financial risk of losing you is insurance. If you’d like to review your current coverage or think through what an income protection strategy should look like for your situation, reach out to Enduring Wealth Advisors.

Important Disclosures:

This article contains only general descriptions and is not a solicitation to sell any insurance product or security, nor is it intended as any financial or tax advice. For information about specific insurance needs or situations, contact your insurance agent. This article is intended to assist in educating you about insurance generally and not to provide personal service. They may not take into account your personal characteristics such as budget, assets, risk tolerance, family situation or activities which may affect the type of insurance that would be right for you. In addition, state insurance laws and insurance underwriting rules may affect available coverage and its costs. Guarantees are based on the claims paying ability of the issuing company. If you need more information or would like personal advice you should consult an insurance professional. You may also visit your state’s insurance department for more information.

Sources: Satish M., et al. “Sex Differences in Outcomes of Young Adults Hospitalized With First Myocardial Infarction From 2011 to 2022.” Journal of the American Heart Association, 2026. Wall Street Journal, February 26, 2026. CDC National Center for Health Statistics. National Academies of Sciences, Engineering, and Medicine.

Research and development of this article involved AI tools; graphics were AI-generated.