Featured Posts

Three Benefits, One Decision: Should My Spouse Claim SS Early While Still Working?

A client recently asked a question I hear regularly. The names have been changed, but the situation is common enough that the answer is worth sharing publicly.

A client recently asked a question I hear regularly. The names have been changed, but the situation is common enough that the answer is worth sharing publicly.

Q: My wife Frances just turned 63. Some of her colleagues are encouraging her to claim her Social Security benefit now and then switch to a survivor benefit on my record when I pass. She plans to keep working part-time. What should we consider?

A: This is a genuinely complex question, Thomas — and Frances’s colleagues aren’t entirely wrong. But there’s quite a bit more to untangle before deciding.

The three benefits Frances could receive

Frances has access to three distinct Social Security benefits, and they interact in ways that aren’t always obvious.

Her own benefit is based on her personal earnings record. A spousal benefit — available once you file — would top up her benefit to 50% of your age 67 (aka Full Retirement Age (FRA)) benefit, minus her own age 67 benefit. And the survivor benefit is the one her colleagues mentioned: if you predecease her, she receives the greater of her benefit or yours, not both.

For the spousal and survivor benefits, your benefit amount matters enormously. In your case, Thomas, you’ve been at or near the Social Security taxable wage base for most of your career. That shapes your benefit significantly — and makes the math worth running carefully.

What claiming at 63 actually costs

Claiming four years before age 67 reduces Frances’s own benefit by approximately 25% and her spousal top-up by approximately 30%. These aren’t temporary reductions. They’re permanent, and every future cost-of-living adjustment (COLA) compounds them.

Here’s an illustrative example. Say your age 67 benefit is $4,000 monthly and Frances’s is $1,000. Her spousal top-up at age 67 would be $1,000 (half of your $4,000 = $2,000, minus her own $1,000 benefit). Claiming at 63 reduces her own benefit to about $750 and the spousal top-up to about $700 — a total of $1,450 monthly instead of $2,000.

Here’s an illustrative example. Say your age 67 benefit is $4,000 monthly and Frances’s is $1,000. Her spousal top-up at age 67 would be $1,000 (half of your $4,000 = $2,000, minus her own $1,000 benefit). Claiming at 63 reduces her own benefit to about $750 and the spousal top-up to about $700 — a total of $1,450 monthly instead of $2,000.

By the time Frances reaches her mid-70s, the larger monthly benefits from delaying have overtaken the balances

received by claiming early. By her mid-80s, she’s about $65,000 ahead by delaying, and that grows to about $140,000 if you both live to your mid-90s.

These numbers use the illustrative benefit amounts above. The only way to know the real numbers is to have your actual Social Security Statements in hand.

The earnings test: why working changes the math

Frances still plans to work, and that matters. In 2026, the Annual Earnings Test (AET) exemption is $24,480. If she earns more than that before reaching age 67, Social Security withholds $1 in benefits for every $2 of excess earnings. Withheld benefits aren’t lost forever — they get credited back as a slightly higher benefit at age 67 — but it complicates cash flow planning and reduces the near-term value of claiming early.

If Frances’s income stays around $24,000–$25,000 annually, she likely stays within the exempt amount, and the earnings test isn’t a significant concern.

The case for claiming early

There is one. If she claims now and stays below the AET limit, she’d collect roughly $750 monthly for four years — approximately $36,000 in cumulative benefits before any COLA adjustments. If she can invest those proceeds — particularly in a Roth IRA, since she has earned income — the case becomes stronger, as tax-free compounding adds real value to the early-claiming strategy.

The case for waiting

Our general planning philosophy treats delayed Social Security claiming as longevity insurance. It’s a government-guaranteed benefit, indexed to inflation, that neither of you can outlive. The survivor receives the full amount — which is especially meaningful for a surviving spouse facing potentially 25 to 30 years on a single income.

Because you’re the higher earner, Thomas, the most important long-term move is for you to delay to 70. That maximizes the benefit Frances would receive as your survivor for potentially decades. Staying active and healthy — as we discussed in Stay in Your Prime Longer: Why Active Retirees Enjoy 15 More Years of Independence — directly affects how long that survivor benefit matters, which is why the two decisions are connected.

For Frances specifically, whether delaying her own benefit is worth it depends on how large that benefit actually is, how it interacts with the spousal top-up, and what bridge income you’d use in the meantime. Which brings us back to the Statements.

A security note worth acting on today

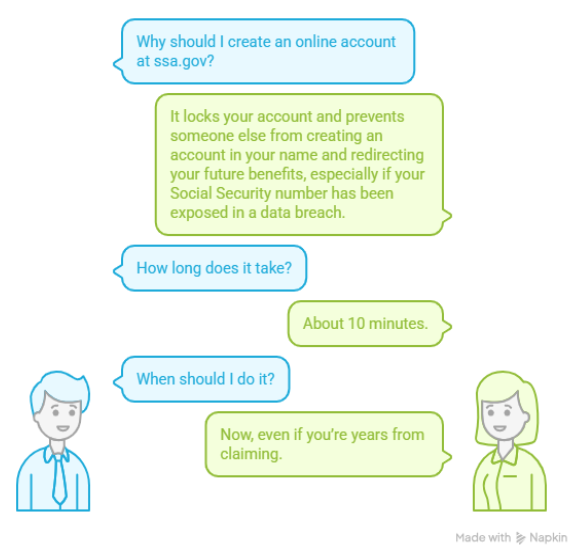

If either of you has never created an online account at ssa.gov, do it now — even if you’re years from claiming. Once your Social Security number has been exposed in a data breach (and statistically, it probably has been), someone else could create an account in your name and redirect your future benefits. Creating your account first locks it. It takes about 10 minutes and is one of the simplest protective steps you can take.

What we’d want to know before finalizing anything

Leading academic research — and the Social Security Administration itself — has found that for people with normal life expectancies, the lifetime value of benefits is roughly similar across claiming ages. The difference comes down to longevity assumptions, investment returns, and how the survivor benefit interacts with each strategy. Since both of you expect long lives, delayed claiming tends to come out ahead once survivor protection is factored in.

But we can’t actually know which strategy works better for your household without Frances’s projected benefit, your projected benefit, and the numbers from your Social Security Statements. If you don’t have them handy, we can access them together. That 20-minute conversation could be worth six figures over a lifetime.

Research and development of this article involved AI tools; graphics were AI-generated.

How one Couple gets the most out of Social Security

by Ralph Bender, MBA, CFP®

Randy loves the business he’s created. It was very difficult getting started, with no capital, three young kids. But the family rallied around him, helped him find good clients, and they survived. The longer he works in the business, the easier it gets to attract business…

Four Ways to Handle Your Future Long-Term Care Expenses

by Ralph Bender, MBA, CFP®

Half of us will need help with activities like bathing, dressing or eating sometime in our futures; the rest of us will die before needing such Long Term Care (LTC). With at least a 50% chance of needing LTC, it is important to have a plan for obtaining the care before you are most vulnerable…

Featured Market Volatility

Investing With Tariffs In Mind

by Ralph Bender, MBA, CFP®

Tariffs—taxes imposed on imported goods—have become an essential factor for investors to consider. They are typically used to protect domestic industries from foreign competition by increasing the costs of imported goods…

Teetertotter Market or Wall of Worry?

by Ralph Bender, MBA, CFP®

GrandpaLand is a swing, trampoline, hammock, and a teetertotter in the shaded corner of our back yard. On Thursdays, the “littles,” as we call the grandkids under seven, spend the day with Grandma, while their respective parents get some work done…

Running Money® On the Trail – Don’t Get Bit

by Ralph Bender, MBA, CFP®

It was a little guy, about a foot long, just stretched out across the main trail. I was two steps beyond him before stopping, realizing it’s the first I’ve seen this season. Experienced runners develop a “sixth sense” about their footfalls…

Featured Financial Planning

")

You’re Too Young to Think About Dying — That’s Exactly the Problem

by Ralph Bender, MBA, CFP®

“Tariffs—taxes imposed on imported goods—have become an essential factor for investors to consider. They are typically used to protect domestic industries from foreign competition by increasing the costs of imported goods…

Three Benefits, One Decision: Should My Spouse Claim SS Early While Still Working?

by Ralph Bender, MBA, CFP®

A client recently asked a question I hear regularly. The names have been changed, but the situation is common enough that the answer is worth sharing publicly…

How to Align the Levers of Your Retirement

by Ralph Bender, MBA, CFP®

“Knock three times on the ceiling if you want me; twice on the pipe if the answer is no.”

I haven’t heard that song in years. Why is it rattling around my brain for the past 24 hours? Oh, wait! Maybe it did play on the 70’s channel I tuned in while driving last week. That must have been the trigger that gave me this earworm…

Featured Lifestyle

Book Review: The Man Who Knew

Review by Ralph Bender, MBA, CFP®

I thought I knew Alan Greenspan. After all, I lived through his entire tenure at the Fed, watched him testify before Congress, and experienced the economic cycles he helped shape. Turns out, I didn’t know him nearly as well as I thought. Sebastian Mallaby’s “The Man Who Knew” reveals a far more complex and fascinating figure than the measured, almost robotic Fed chairman who appeared on our television screens….

Recipe: Mark’s Version of Pioneer Woman’s Potato Soup

by Mark R Tracy, MBA, CFP®

½ to 1 lb. of raw bacon, diced

1 cup of diced onions

1 cup of diced carrots…

Fitness: The Age-Proof Brain

Review by Ralph Bender, MBA, CFP®

In “The Age-Proof Brain,” Marc Milstein provides an easy-reading yet highly informative guide to maintaining a healthy and sharp mind throughout life. Milstein, a neuroscientist, skillfully combines the latest scientific research with practical advice, creating a comprehensive guide to cognitive well-being…

Most Recent

Year-End Planning for Retirees

by Mark R Tracy, MBA, CFP®

As we approach the coming year, let’s look at year-end planning for your finances…

TALKING TO YOUR CHILDREN ABOUT INHERITANCE – Checklist

by Mark R Tracy, MBA, CFP®

If you feel uneasy chatting with your kids or grandkids about money, trust me, you’re not alone. Many parents find discussing inheritance with their children to be quite a challenge…

Forward-Thinking Investors Get Triple-Tax-Advantage from Healthcare Savings Accounts

By Ralph Bender, MBA, CFP®

We just finished the longest bear (down) market since Elvis’ “Jailhouse Rock” was a top hit. (That was 1957-58.) How did we finish a bear market? As a reminder, a bear market is a drop of more than 20% from a recent highwater mark. From January through October last year, the S&P 500 index dropped 24%.

Blog Search

Get Our Newsletter

Schedule A Call

Securities are offered through LPL Financial, Member FINRA / SIPC. Investment advice offered through Enduring Wealth Advisors®, LLC, a registered investment advisor. Enduring Wealth Advisors®, LLC and Enduring Wealth, Inc are separate entities from LPL Financial.

The LPL registered representatives of Enduring Wealth Advisors® may only discuss securities or transact business with persons who are residents of AR, AZ, CA, CO, ID, KS, KY, LA, MN, NH, NM, NV, OH, OK, OR, PA, SC, SD, TX, UT, VA, WA, WV.

No information provided on this site is intended to constitute an offer to sell or a solicitation of an offer to buy shares of any security, nor shall any security be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under securities laws of such jurisdiction.

EnduringWealth.com and Enduring Wealth Advisors® its content, links, and excerpts may be used with clear credit and attribution. Unauthorized use is prohibited.